BETA’s ALIA sale precursor of BIG electric RAM market? Where, why, and when?

Some really smart analysts[1] are forecasting that Faye Malarkey Black and RAA should be hiring staff to be able to serve growth in their members and operations. WHY??? The global market for Regional Aircraft Market (RAM) [assuming that the vehicles will be electric)could reach $75-115B by 2035, with the US potentially capturing 25-35% of that, so about $20-35B in ten years.

be electric)could reach $75-115B by 2035, with the US potentially capturing 25-35% of that, so about $20-35B in ten years.

But these planes require recharging and that shortens the daily flight time-NO?

5–40% of the aircraft’s duty day is effectively “consumed” by charging or battery‑swap time, depending on:

-

-

-

- How much charging can be overlapped with normal turn activities

- Whether you use hot‑swap packs vs. plug‑in fast charge

- Ambient temperature and battery longevity constraints

-

-

With well‑designed battery swap systems, you could push that down:

-

-

-

- Swap time: 10–15 minutes

- Charging done off‑aircraft in parallel

-

-

→ Effective “charging penalty” could drop to 10–20% of the day.

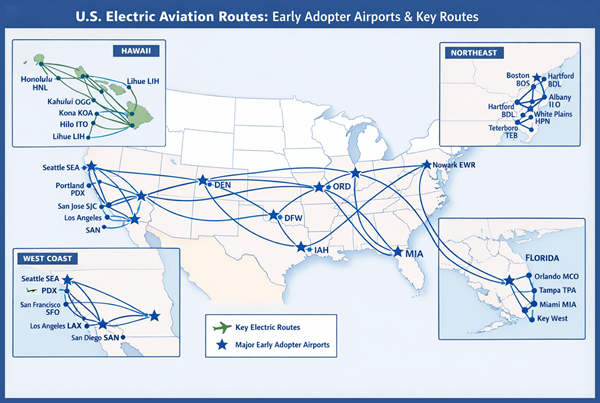

Where would these electric birds fly? To which markets will they be deployed?

US regions and point‑to‑point patterns

US regions and point‑to‑point patterns

-

-

-

- Northeast corridor

- Use case: Avoid congested highways and hubs; connect secondary cities.

- Likely routes (illustrative, not exhaustive):

- Boston–Portland (ME), Boston–Albany, Boston–Hartford

- Summer operations- the Cape, Islands, ME/NH/VT/

- NYC area (HPN/TEB/ISP)–Albany, Syracuse, Hartford, Providence

- Philly–Harrisburg, Philly–Allentown, DC–Richmond, DC–Norfolk (stretch)

- Why it works:

- High value of time, chronic road congestion, many underused regional airports.

- Strong policy and corporate pressure on decarbonization.

- California and West Coast

- Likely routes:

- Bay Area (OAK/SJC/PAO)–Monterey, Santa Rosa, Sacramento, Fresno

- LA basin–Palm Springs, Santa Barbara, San Diego (short legs)

- Vegas

- PNW: Seattle–Bellingham, Seattle–Yakima, Portland–Eugene

- Drivers:

- Strong climate policy, tech‑friendly early adopters, dense regional airport network.

- Northeast corridor

-

-

-

-

-

- Hawai’i

- SurfAir Launch customer of Alia

- Quiet flight will increase likelihood of sightseeing flights near National Parks

- State will see this as win-win:

- Reinstatement of flights (economy) almost zero noise impact

- Hawai’i

-

-

-

-

-

- Texas triangle and Gulf

- Likely routes:

- Dallas–Waco, Dallas–Tyler, Dallas–Abilene

- Houston–College Station, Houston–Beaumont

- San Antonio–Austin, Austin–Killeen

- Drivers:

- Business travel, oil & gas, university and medical traffic, long road drives with predictable demand.

- Florida and Southeast

- Likely routes:

- Orlando–Tampa, Orlando–Daytona, Orlando–Melbourne

- Miami–Key West, Miami–Naples, Miami–Fort Myers

- Atlanta–Chattanooga, Atlanta–Greenville, Charlotte–Asheville

- Drivers:

- Tourism, leisure, cruise connections, snowbird traffic, weather‑sensitive but high volume.

- Counter seasonal option for Northeast summer flights

- Rural and underserved communities

- Use case: Restore or enhance connectivity where RJs and turboprops are uneconomic.

- Patterns:

- Spokes into regional hubs:

- g., Denver–rural CO, Salt Lake–regional UT/ID, Minneapolis–Upper Midwest, Anchorage–Alaska communities (with range caveats).

- Essential Air Service–like missions:

- Thin routes where low operating cost and quiet operations matter more than speed.

- Spokes into regional hubs:

-

-

In terms of where electric wins first,

- short‑haul, high‑yield corridors near major metros (NE, CA, TX, FL)

But will there be adequate revenues for these flights?

Very approximate, but to give shape:

-

-

-

-

-

- Northeast & Mid‑Atlantic:

$1.5–4B/year (dense demand, high yields) - California & West Coast:

$1–3B/year - Texas & Central/South:

$1–3B/year - Florida & Southeast:

$1–2B/year - Rural/Frontier (Midwest, Rockies, Alaska, etc.):

$0.5–2B/year

- Northeast & Mid‑Atlantic:

-

-

-

-

Total lines up with the earlier $5–15B/year US electric RAM estimate.

So can these RAM carriers start flying now? Soon?

Electric aircraft require megawatt‑scale charging, major grid upgrades, new safety protocols, and standardized charging systems—infrastructure that most airports do not yet have

-

-

-

-

- Electric regional aircraft (9–30 seats) will require 5–3 MW chargers to support fast turnarounds.

- This is far beyond what current GA or regional terminals can supply.

- Airports and airlines cannot fund this alone—coordinated investment is required.

- Many regional airports have limited grid capacity (often <1 MW total).

- Utilities require multi‑year planning for substation upgrades.

- High‑power charging introduces thermal management and safety

- Airports need new substations, transformers, and high‑capacity feeders.

- Grid upgrades often take 3–7 years, longer than aircraft certification timelines.

- Electric aircraft adoption will also coincide with electrification of:

- Ground support equipment

- Shuttle buses

- Rental car fleets

- Airport buildings

(All competing for the same electrical headroom.)

- Lack of Standardized Charging Interfaces

- No universal standard yet for:

- Voltage levels

- Connector types

- Communication protocols

- Safety interlocks

- Without standards, airports risk installing stranded assets.

- Safety, Fire, and Thermal Management

- Lithium‑ion battery systems require:

- Dedicated fire suppression zones

- Thermal runaway containment

- New NFPA and FAA procedures

-

-

-

-

-

-

-

-

-

- Ground crews must be trained in:

- High‑voltage systems

- Battery handling

- Emergency response

- Ground crews must be trained in:

-

-

-

-

-

-

-

-

-

- Airports must redesign ramp areas to accommodate battery swap bays or charging pads.

-

-

-

- Operational Integration Challenges

-

-

-

-

-

- Charging time affects gate/stand utilization.

- Airports must redesign:

- Turn‑time workflows

- Ground crew training

- Emergency response procedures

-

-

-

-

Airports already preparing:

-

-

-

-

-

- Seattle–Tacoma (SEA)

- Los Angeles (LAX)

- San Francisco (SFO)

- San Diego (SAN)

- Boston (BOS)

- Concord, NH

- Modesto, CA

- Fresno, CA

- Paine Field (PAE), WA

- Springfield–Branson, MO

-

-

-

-

President Trump’s Secretary of Transportation Duffy’s eIPP has established implementation goals for certificating RAM(and other) aircraft types, for authoring air carrier operations with them and for approving the airport infrastructure-

Will eIPP hasten the eVTOL Future?

The states, airports, OEMs, and carriers in eIPP already are preparing for this new electric flight vision as soon as THIS YEAR. For states/airlines/airports not moving toward the demand of these greener forms of air transportation, THERE’S MUCH THAT NEEDS TO BE DONE (9 months?). Economic Development is on every government’s active agenda and RAM poses an opportunity

-

-

-

-

-

- for HIGH PAYING JOBS,

- new air services tend to stimulate local economies

- visitors

-

-

-

-

Does your State want to attract an Advanced Aerial Mobility Company – high paying jobs and sales???

Making your airport attractive for this increase in flights, requires attracting a new airline and/or encouraging an incumbent to acquire RAM equipment. Neither of those options will be viewed as realistic by a prospective electric carrier UNTIL you have made concrete steps in implementation. Help in

-

-

-

-

-

- dealing with the airport certification ,

- anticipating the needed infrastructure

-

-

-

-

and

-

-

-

-

-

- coordinating with the RAM tenant

-

-

-

-

Surf Air orders BETA Technologies’ all-electric ALIA for Hawaii pax flights

Miquel Ros March 15, 2026

BETA TECHNOLOGIES announced on March 12, 2026, that it has signed a strategic partnership with SURF AIR MOBILITY, a regional air transportation operator based in the United States.

Surf Air Mobility has placed a firm order for 25 of BETA Technologies’ all-electric CTOL (conventional takeoff and landing) aircraft plus 75 options.

With this agreement, Surf Air Mobility will not only become BETA Technologies’ launch customer for passenger flights, but also the exclusive service center for the company’s aircraft in some designated geographical regions.

The first of these regions will be Hawaii, where Surf Air Mobility operates an extensive inter-island network through its subsidiary Mokulele Airlines, which operates a fleet of 18 Cessna 208EX Grand Caravan commuter aircraft.

The first of these regions will be Hawaii, where Surf Air Mobility operates an extensive inter-island network through its subsidiary Mokulele Airlines, which operates a fleet of 18 Cessna 208EX Grand Caravan commuter aircraft.

The two companies have also agreed to conduct a series of demonstration flights with the ALIA in Hawaii before the end 2026 and to work together to promote the adoption of new generation aircraft with the launch of joint marketing and communication campaigns.

The agreement is conditional on BETA Technologies completing its certification process with the Federal Aviation Administration (FAA), which is currently underway.

BETA Technologies has also recently completed testing and evaluation campaigns in Norway and New Zealand. These overseas tests have been conducted together with BETA Technologies’ partners Bristow Group and Air New Zealand, respectively.

BETA Technologies co-founder and CEO shows us around the CX300 ALIA aircraft

[1] Regional Air Mobility Market Research Report 2025-2034;; Regional air mobility: A short-range flight renaissance? | McKinsey; (10) Regional Air Mobility Market Insights, Adoption, Technology Trends, & Forecast to 2034 | LinkedIn