FLYING CARS a/k/a eVTOLs- past certification, future technical and financial challenges

![]() has published a financial review entitled “Flying Cars and Rising Bars: The 2026 eVTOL Breakout Begins”. The prospects of five ‘leading” OEMs in this sector. While some of the comments mention operational aspects, the primary focus is investment risk.

has published a financial review entitled “Flying Cars and Rising Bars: The 2026 eVTOL Breakout Begins”. The prospects of five ‘leading” OEMs in this sector. While some of the comments mention operational aspects, the primary focus is investment risk.

Nothing in aviation is new; not really-the short excerpt about the CAA’s certification of a flying car makes the innovative eVTOL design a second generation (sort of).↓↓↓

A summary of aeronautical technical journals has created an outline of the major hurdles facing U.S. eVTOL adoption—manned and unmanned—grounded in the latest reporting and regulatory developments.

Technical & Engineering Hurdles

Novel Flight Modes & Distributed Propulsion

-

- eVTOLs combine powered‑lift, tiltrotor‑like transitions, and distributed electric propulsion, creating engineering complexity far beyond traditional Part 23/27 aircraft.

- Transition flight (hover → forward flight → hover) remains the most difficult domain to validate for safety and reliability.

-

-

- V‑22 Osprey’s military operations suffered from a persistent mix of mechanical complexity, high maintenance burden, and reliability shortfalls that undermine their promised speed‑and‑range advantages.

-

- Battery Energy Density & Thermal Management

-

- Current lithium‑ion chemistries limit:

- Range

- Payload

- Reserve requirements

- Turnaround time (charging vs. battery swap)

- Thermal runaway and crashworthiness requirements add further design burdens.

- Current lithium‑ion chemistries limit:

- Software & Fly‑By‑Wire Assurance

-

- High‑integrity flight control laws must meet DO‑178C/DO‑254‑level rigor.

- Distributed propulsion requires fault‑tolerant architectures that are still maturing.

- Industrialization & Late‑Stage Burn

-

- As CleanTechnica notes, late‑stage certification, and production scale‑up cause steep cash‑burn curves, including:

- Conforming aircraft builds

- Destructive testing

- Environmental qualification

- Supplier traceability

- Production tooling

- As CleanTechnica notes, late‑stage certification, and production scale‑up cause steep cash‑burn curves, including:

Certification Hurdles (FAA)

- Powered‑Lift Certification Under §21.17(b)

- FAA has created a pathway (Advisory Circular 21.17‑4, 2025), but powered‑lift is still a novel category, requiring custom airworthiness criteria.

- Means of Compliance (MOCs) acceptance has taken years for Joby and Archer.

- Performance‑Based Standards

-

- FAA is shifting toward performance‑based rules, but this requires:

- New test methods

- New safety interpretations

- Extensive data collection

- FAA is shifting toward performance‑based rules, but this requires:

- Human Factors & Autonomy

- For MANNED AIRCRAFT: pilot workload, energy‑state awareness, and transition‑mode symbology remain open issues (e.g., Joby’s remaining MOCs relate to charge‑status communication).

- For UNMANNED AIRCRAFT: no established pathway yet for autonomous passenger‑carrying operations. (NOTE: the DOT eIPP includes autonomous tests)

-

- Long‑Tail Certification Timelines

-

- Reference‑class forecasting (CleanTechnica) suggests novel aircraft categories often face significant schedule overruns, similar to the AW609 tiltrotor.

Infrastructure Hurdles

- Vertiport Build‑Out

- U.S. lacks standardized, certificated vertiports.

- Challenges include:

- Zoning

- Fire safety for high‑energy batteries

- Rooftop structural reinforcement

- Passenger processing and emergency egress

??? will FAA standards preempt local standards for these facilities???

- Grid Capacity & Megawatt‑Scale Charging

- Many U.S. airports—especially regionals—lack the electrical capacity for:

- Fast charging

- Multiple simultaneous aircraft

- Thermal management and charging‑interface standardization remain unresolved.

- Air Traffic Integration

- Many U.S. airports—especially regionals—lack the electrical capacity for:

-

- Integrating thousands of low‑altitude eVTOL flights into already congested urban airspace is a major hurdle.

- UTM (Uncrewed Traffic Management) and ATM (Air Traffic Management) systems are not yet interoperable at scale.

Economics & Consumer Elasticity of Demand

- High Operating Costs (Near‑Term)

- Battery replacement cycles, maintenance of distributed propulsion, and vertiport fees will keep early prices high.

- U.S. consumers have limited willingness to pay for short‑range premium mobility unless:

- Time savings are substantial

- Reliability is high

- Safety is unquestioned

- Uncertain Business Models

-

- Air taxi economics depend on:

- High utilization

- Autonomous operations (long‑term)

- Low‑cost energy

- Without autonomy, pilot labor costs may make manned eVTOLs uncompetitive with premium ground transport.

- Air taxi economics depend on:

- Price Elasticity Differences: Manned vs. Unmanned

- Manned eVTOLs: Compete with Uber Black, helicopters, and premium rail; elasticity is high—small price increases reduce demand.

- Unmanned cargo eVTOLs: More resilient demand; cost savings vs. trucks/drones may justify adoption.

Public Acceptance & Noise

- Noise signatures (tonal, high‑frequency) remain unfamiliar to communities.

- Public acceptance is tied to:

- Safety record

- Crash survivability

- Visual clutter

- Privacy concerns (for unmanned)

- Public acceptance is tied to:

Regulatory & Operational Hurdles Beyond Certification

- Operational Rules for Powered‑Lift

- FAA finalized powered‑lift operational rules in 2024, but:

- Pilot training standards

- Route approvals

- Weather minima

- Maintenance rules

are still evolving.

- FAA finalized powered‑lift operational rules in 2024, but:

-

- Insurance & Liability

-

- No actuarial history exists for eVTOL operations.

- Insurers may price risk conservatively, raising operator costs.

-

- Integration with Existing Airport Operations

-

- Gate utilization, ground crew workflows, and safety zones must be redesigned for electric aircraft.

Unmanned‑Specific Hurdles

- No U.S. regulatory pathway yet for autonomous passenger‑carrying aircraft.

- Detect‑and‑avoid requirements for dense urban environments remain unsolved.

- Cybersecurity and command‑and‑control link reliability must meet extremely high assurance levels.

Need help working through the regulatory maze or would like insights into specific eVTOL designs? Click here.

Excerpted click on link for full article

Flying Cars and Rising Bars: The 2026 eVTOL Breakout Begins

Written by Jeffrey Neal Johnson

- Vertical Aerospace is preparing to showcase its flagship aircraft to institutional investors in New York City later this month.

- Industry leaders Joby Aviation and Archer Aviation are advancing rapidly toward commercial launch with new flight simulators and manufacturing progress.

- The transition from research and development to full-scale commercial operations is driving renewed investor confidence across the entire electric aviation market.

- Five stocks to consider instead of Vertical Aerospace.

The January Effect has arrived in the aerospace sector, and it is electric. [bad pun!!!]

After a year defined by rigorous flight testing and capital-intensive research, the Electric Vertical Takeoff and Landing (eVTOL) sector is witnessing a sharp rotation of capital back into growth stocks. As the calendar flips to 2026, investors are betting that the industry is graduating from a science project to a commercial reality.

[1/26 financial date deleted.]

For investors, the narrative has shifted. The question is no longer: Will this technology work? Physics has already proven it can. The questions for 2026 are: Who enters service first? And who has the best go-to-market strategy? The market is starting to price in the expectation that commercial passenger flights are months, not years, away. After a long climb through the overcast skies of regulatory oversight, the sector is finally emerging from the fog, with clearer skies in sight.

The Valo Debut: Vertical Aerospace Takes Manhattan

VERTICAL AEROSPACE Today

[1/26 financial date deleted.]

Perhaps the most notable story of the week belongs to Vertical Aerospace. Previously viewed by some analysts as a volatility play due to liquidity concerns, the company is actively reshaping its narrative to start the year.

Vertical’s stock climbed 12% following a flurry of strategic updates that challenge the perception of the company as a laggard. The company recently rebranded its flagship aircraft, the VX4, as Valo, and announced a US Tour launching this month. By bringing the hardware physically to New York City, Vertical is signaling confidence to institutional investors. This is a show-me move designed to prove that the aircraft is ready for the global stage.

Securing the Runway: The Jan. 20 EGM

Beyond the marketing push, Vertical is taking tangible steps to secure its financial future. The company will hold an Extraordinary General Meeting (EGM) on Jan. 20, 2026, in Bristol, UK. The agenda is focused on increasing the company’s authorized share capital.

For new investors, this is a critical detail:

- What it means: It allows the company to issue more shares of stock.

- Why it matters: While this can dilute existing shareholders, in this context, the market is interpreting it as a bullish signal for survival. It creates the mechanism for Vertical to receive necessary funding, potentially from the recent Mudrick Capital deal or new strategic partners.

It suggests management is preparing to scale operations, not wind them down. Additionally, investors are buying ahead of a major technical catalyst: the Transition Flight. Expected in the first quarter of 2026, this test will see the aircraft transition from vertical hovering to wing-borne flight. Successful execution of this maneuver is the most critical engineering hurdle remaining for the British manufacturer.

Simulators and Factories: How the Leaders Are Executing

While Vertical captures the speculative upside, Joby Aviation and Archer Aviation remain the standard-bearers for stability. Both stocks have been trending up over the past five days, reflecting a flight to quality within the growth sector.

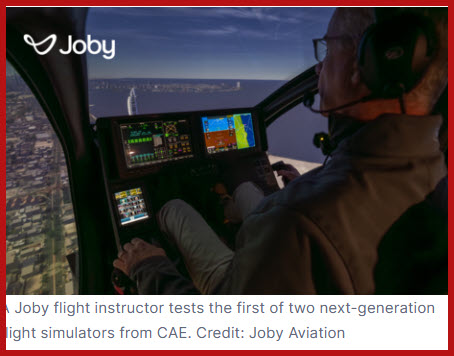

Joby’s Training Milestone

JOBY AVIATION Today

[1/26 financial date deleted.]

Joby Aviation continues to validate its position as the sector leader.

In a breaking update on Jan. 6, JOBY accepted delivery of FAA-qualified flight simulators from CAE. This update may seem minor compared to flight tests, but it is a massive operational unlock.

An airline cannot launch without trained pilots, and pilots cannot train without certified simulators. By securing this hardware now, Joby is ensuring its pilot pipeline is ready for the planned launch of commercial operations in Dubai later this year.

Financially, Joby remains the strongest in the class, boasting nearly $1 billion in liquidity backed by Toyota NYSE: TM. This cash pile allows them to weather regulatory delays that might bankrupt smaller competitors.

Archer’s Industrial Push

ARCHER AVIATION Today

[1/26 financial date deleted.]

Similarly, Archer Aviation has found stability through its alliance with Stellantis NYSE: STLA. The focus for Archer in 2026 is the industrialization of its Midnight aircraft at its Georgia facility.

Archer completed over 400 test flights in 2024, exceeding its own goals. The company is now routinely flying piloted missions and meeting key performance metrics, including range and altitude.

By leveraging Stellantis for manufacturing, Archer avoids the massive capital expenditure required to build factories alone.

This capital-efficient strategy allows them to focus their cash burn on certification rather than construction.

IPO Cash and Prototype

Flights: BETA and Eve Update

BETA TECHNOLOGIES Today

[1/26 financial date deleted.]

The market landscape has also been permanently altered by the recent arrival of BETA Technologies NYSE: BETA. Following its November 2025 IPO, BETA offers investors a different approach.

Unlike its peers’ focus on urban air taxis, BETA targets cargo and medical logistics first.

With approximately $1 billion in fresh capital from its public listing and a valuation nearing $7.5 billion, BETA is a financial heavyweight.

Their dual-use strategy reduces the immediate pressure of passenger safety regulations, offering a potentially safer, faster path to revenue.

EVE Today

[1/26 financial date deleted.]

Meanwhile, Eve Air Mobility NYSE: EVEX, a spin-off of Embraer NYSE: EMBJ, has silenced critics who claimed it was falling behind.

In December 2025, Eve completed the first flight of its unnamed full-scale prototype.

This milestone moves the company from the design phase to the hardware phase.

Backed by Embraer’s global service network, Eve argues that once certified, it will have the easiest time scaling maintenance and operations globally due to its parent company’s existing supply chain.

Volatility vs. Viability: The Pre-Production Window Closes

EHang Today

[1/26 financial date deleted.]

The synchronized rally in the first week of January signals that the eVTOL sector has graduated. We have moved from the Concept Phase to the Pre-Commercial Phase.

Global benchmarks like EHang NASDAQ: EH, which is ALREADY GENERATING REVENUE FROM COMMERCIAL FLIGHTS IN CHINA, provide the proof of concept that sustains valuations for Western peers. If the business model works in Guangzhou, the logic follows that it will work in New York, Los Angeles, and Dubai.

Guangzhou, the logic follows that it will work in New York, Los Angeles, and Dubai.

For investors, the distinction is vital. The risks are no longer about whether the laws of physics allow these aircraft to fly; we know they can. The risks are now about execution and liquidity.

Joby and Archer offer the most direct path to FAA approval. BETA offers a diversified logistics play. But Vertical Aerospace, with its Valo aircraft heading to New York and a critical technical unlock on the horizon, provides the most dynamic risk-reward profile of the new year. As the US Tour begins, the market is betting that the window to buy these stocks at pre-revenue prices may be closing.